Estates Under $2 Million – Do I Need an Estate Plan?

With the exciting and long overdue news of the increase in the Massachusetts estate tax exemption from $1 million to $2 million for decedents dying on or after January 1, 2023, many Massachusetts residents have been left wondering whether they still need an estate plan. Keep in mind that several of the most critical reasons for having an estate plan in place are not tied to the amount of assets you own. Aside from tax planning, estate plans are executed in order to avoid probate, name persons to handle your affairs in the event of incapacity and provide a structure for timing of when beneficiaries receive their inheritance. Below is a list of items to take into consideration when deciding whether to execute an estate plan.

Identity of Your Assets.

Your home, other real estate, investment accounts, retirement accounts, life insurance, bank accounts, business interests, vehicles and other items of tangible personal property such as furniture, artwork and jewelry are all part of your taxable estate at death. It is important to create an accurate list of your assets and their estimated value in order to create an estate plan that is tailored to your needs. It could be that although you think your estate is below the $2 million dollar filing threshold, that it may be over that amount once you tally all your countable assets. It is especially important for married couples to consider that even though they may each separately own less than $2 million in assets while they are both alive, after the first spouse dies the survivor will likely inherit the assets of their predeceased spouse, resulting in an estate over the filing threshold.

A typical goal of estate planning is probate avoidance. Of particular concern is to avoid passing real estate through probate. While it is possible to name beneficiaries on other assets such as bank accounts, retirement accounts and investment accounts, thus avoiding probate, adding someone else to a deed, such as a child, simply to avoid probate can have unintended and expensive consequences.

Health Care Agents and Attorneys-in-Fact.

Think about whom you would like to manage your affairs during your life if you are unable to care for yourself or manage your finances. This can be, but does not need to be, the same person. You can choose one person to make medical decisions on your behalf and another to make financial decisions. It is important to remember that an estate plan is not only for tax planning purposes but to protect you during your lifetime. If you do not have documents in place naming a health care agent or attorney-in-fact, it may result in costly and invasive court proceedings to appoint a guardian and/or conservator to make medical or financial decisions on your behalf.

Consider Whether Assets Should Be Held in Trust for Your Beneficiaries After Your Death.

It is especially important for persons with young children to consider how assets will be managed for the benefit of their children and at what age their children will be in charge of their inheritance. Even responsible adult children can benefit from the creditor protection that a properly drafted and administered trust can provide in the event of a divorce or lawsuit.

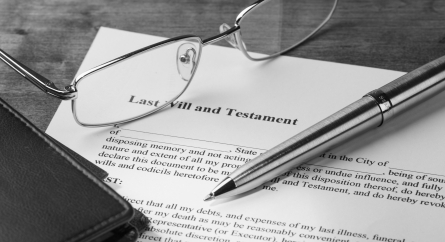

Guardian(s) for Your Children.

If you have minor or otherwise legally incapacitated children, a will is the appropriate document in which to designate guardian(s) for your children. It is good practice to have alternate guardians named as well. The person acting as guardian of your children is not necessarily the person who will have control over the assets that you leave for your children. Sometimes the best caregiver for your children is not necessarily the most appropriate person to handle finances.

The bottom line is that everyone needs an estate plan regardless of their net worth.

Tagged In: estate planning, health care agent, inheritance, Massachusetts estate tax exemption, taxable estate